Your credit report contains information about your past and present credit transactions. It's used primarily by potential lenders to evaluate your creditworthiness. So if you're about to apply for credit, especially for something significant like a mortgage, you'll want to get and review a copy of your credit report.

You can see what they see: getting a copy of your credit report

Every consumer is entitled to a free credit report every 12 months from each of the three credit bureaus: Experian, TransUnion, and Equifax. Besides the annual report, you are also entitled to a free report under the following circumstances:

- A company has taken adverse action against you, such as denying you credit, insurance, or employment (you must request a copy within 60 days of the adverse action)

- You're unemployed and plan to look for a job within the next 60 days

- You're on welfare

- Your report is inaccurate because of fraud, including identity theft

Visit www.annualcreditreport.com for more information.

What's it all about?

Your credit report usually starts off with your personal information: your name, address, Social Security number, telephone number, employer, past address and past employer, and (if applicable) your spouse's name. Check this information for accuracy; if any of it is wrong, correct it with the credit bureau that issued the report.

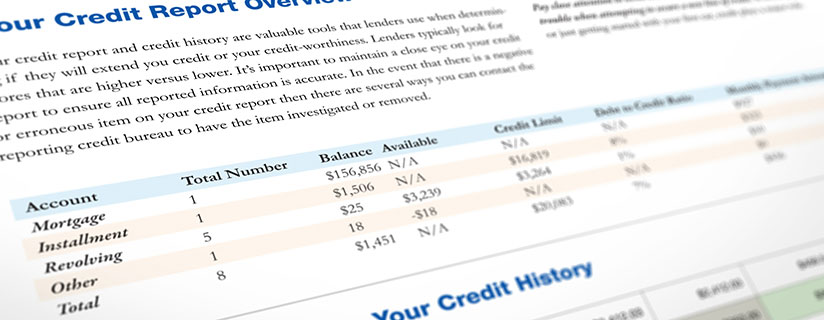

The bulk of the information in your credit report is account information. For each creditor, you'll find the lender's name, account number, and type of account; the opening date, high balance, present balance, loan terms, and your payment history; and the current status of the account. You'll also see status indicators that provide information about your payment performance over the past 12 to 24 months. They'll show whether the account is or has been past due, and if past due, they'll show how far (e.g., 30 days, 60 days). They'll also indicate charge-offs or repossessions. Because credit bureaus collect information from courthouse and registry records, you may find notations of bankruptcies, tax liens, judgments, or even criminal proceedings in your file.

At the end of your credit report, you'll find notations on who has requested your information in the past 24 months. When you apply for credit, the lender requests your credit report--that will show up as an inquiry. Other inquiries indicate that your name has been included in a creditor's prescreen program. If so, you'll probably get a credit card offer in the mail.

You may be surprised at how many accounts show up on your report. If you find inactive accounts (e.g., a retailer you no longer do business with), you should contact the credit card company, close the account, and ask for a letter confirming that the account was closed at the customer's request.

Basing the future on the past

What all this information means in terms of your creditworthiness depends on the lender's criteria. Generally speaking, a lender feels safer assuming that you can be trusted to make timely monthly payments against your debts in the future if you have always done so in the past. A history of late payments or bad debts will hurt you.

Based on your track record, a new lender is likely to turn you down for credit or extend it to you at a higher interest rate if your credit report indicates that you are a poor risk.

Too many inquiries on your credit report in a short time can also make lenders suspicious. Loan officers may assume that you're being turned down repeatedly for credit or that you're up to something--going on a shopping spree, financing a bad habit, or borrowing to pay off other debts. Either way, the lenders may not want to take a chance on you.

Your credit report may also indicate that you have good credit, but not enough of it. For instance, if you're applying for a car loan, the lender may be reviewing your credit report to determine if you're capable of handling monthly payments over a period of years. The lender sees that you've always paid your charge cards on time, but your total balances due and monthly payments have been small.Because the lender can't predict from this information whether you'll be able to handle a regular car payment, your loan is approved only on the condition that you supply an acceptable cosigner.

Correcting errors on your credit report

Under federal and some state laws, you have a right to dispute incorrect or misleading information on your credit report. Typically, you'll receive with your report either a form to complete or a telephone number to call about the information that you wish to dispute. Once the credit bureau receives your request, it generally has 30 days to complete a reinvestigation by checking any item you dispute with the party that submitted it. One of four things should then happen:

- The credit bureau reinvestigates, the party submitting the information agrees it's incorrect, and the information is corrected

- The credit bureau reinvestigates, the party submitting the information maintains it's correct, and your credit report goes unchanged

- The credit bureau doesn't reinvestigate, and so the disputed information must be removed from your report

- The credit bureau reinvestigates, but the party submitting the information doesn't respond, and so the disputed information must be removed from your report

You should be provided with a report on the reinvestigation within five days of its conclusion. If the reinvestigation resulted in a change to your credit report, you should also get an updated copy.

You have the right to add to your credit report a statement of 100 words or less that explains your side of the story with respect to any disputed but unchanged information. A summary of your statement will go out with every copy of your credit report in the future, and you can have the statement sent to anyone who has gotten your credit report in the past six months. Unfortunately, though, this may not help you much--creditors often ignore or dismiss these statements.

Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, legal, or retirement advice or recommendations. The information presented here is not specific to any individual's personal circumstances.

To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances.

These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable — we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.